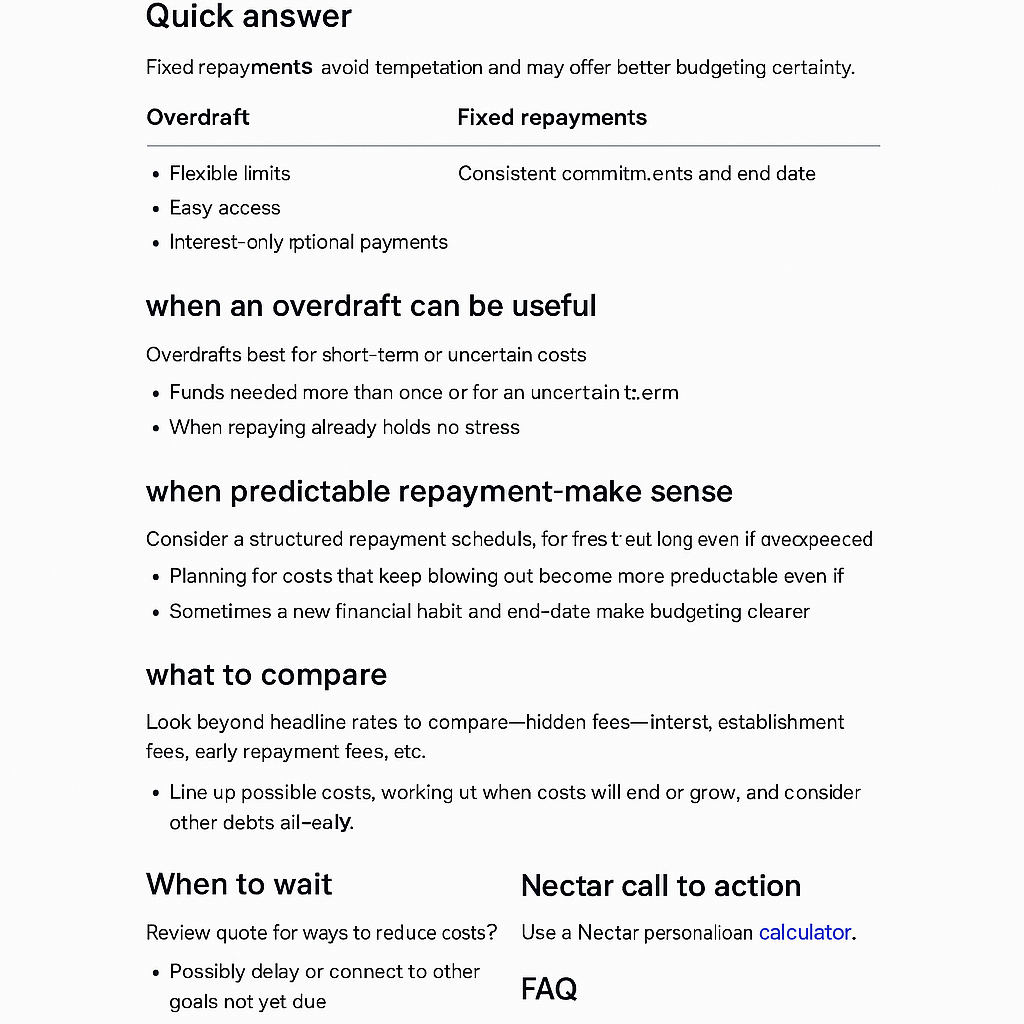

When you’re surprised by a one-off expense—like a mechanical breakdown, insurance excess, or replacing an essential appliance—it’s tempting to dip into your overdraft or swipe the card. But not all borrowing fits every situation. For New Zealanders who don’t want loan stress added to their budget, choosing between a variable overdraft and a fixed personal loan isn’t just about access, but about control and the risk of fees stacking up.

An overdraft is a facility linked to your transaction account. You can use it whenever you like (up to your limit), only paying interest on what you use. This is great for temporary shortages or when the expense disappears in a pay cycle or two. But many New Zealanders find that overdraft debt lingers, gets topped up by other spending, and accumulates fees that can be hard to track day-to-day.

A personal loan with fixed repayments makes it crystal clear what you’ll pay and for how long. You know the cost, you know when it ends, and you can plan your budget around it. For irregular but essential expenses—think WOF failures needing major work, a medical specialist bill, or a large insurance excess—having structure can mean less stress and fewer surprises.

You can’t just look at the advertised interest rate. Here’s what really moves the needle in New Zealand:

If you know when you’ll pay it back, and it’s very soon, an overdraft might be practical. But for any expense that risks lingering, fixed repayments usually cost less in the end and give you back control.

| Situation | Usually better fit | Why or trade-off |

|---|---|---|

| A small, one-off expense (under a week’s bridge) | Overdraft | Flexibility, pay interest only on what you use, quick to clear |

| Large or unpredictable car repair | Fixed repayments | Easier to budget, defined end date, avoids escalating fees |

| Medical bill/insurance excess | Fixed repayments | Certainty, structure, prevents long-term balance creep |

| Frequent dipping in and out of overdraft | Fixed repayments | Habitual use often leads to higher costs and unclear balances |

| Very short-term cash timing issue | Overdraft | Minimal interest if cleared almost immediately |

| Unexpected household appliance replacement | Fixed repayments | One-off, can budget, structure recovery |

| Unsure when or if you can repay | Consider other options | Risk of fees, debt sticking around—delaying or reducing expense may help |

A regional commuter finds their WOF fails due to major brake and suspension issues. The local mechanic advises repairs that can’t be delayed—a safety or insurance rule. The bill will be large and must be paid to get the car back on the road, but there’s only a small saving buffer. The commuter’s choices:

Mid-article call to action:

If you’re facing an unexpected bill and want to see how fixed-term repayments might fit your situation, use Nectar’s loan calculator or check your rate—personalised loan quotes may be available in as little as 7 minutes, depending on the information you provide.

Borrowing isn’t always the smartest move, especially for expenses that are wanted, not strictly needed, or can be spread out. Consider these alternatives:

Hasty borrowing to cover wants, or extending the cost beyond its usefulness, can mean paying more than the expense is worth.

Nectar offers structured personal loans to New Zealanders wanting a clear repayment plan for one-off or irregular expenses. If you’re weighing an overdraft against a fixed loan, Nectar’s digital loan quote tool is quick—personalised loan quotes may be available in as little as 7 minutes, depending on the information you provide.

No set-up or recurring fee surprises—check rates and terms up front (see our rates). Our online calculator helps you see the full cost and pick a loan term and repayment that fits your actual budget.

You won’t get pressure to borrow for things you could delay or avoid. And if a fixed loan seems right, you’ll see transparent fees and a schedule that lets you plan your repayments. Responsible lending means Nectar checks your ability to repay, but our paperless application process streamlines the assessment—reducing friction without cutting corners.

Ready to compare your options for a one-off expense? Start at Nectar.

If you can repay the full amount quickly (weeks, not months) and avoid extra spending, the daily interest can be minimal. Overdrafts get expensive if the balance lingers.

No. For tiny or temporary gaps, the structure of a loan can be overkill. But for anything that can’t be paid back quickly, or where fees could creep up, fixed-term loans usually add clarity and control.

Using an overdraft as a long-term habit makes budgeting tough. Fees and interest are less visible—so overall cost can quietly rise without your noticing. Lenders may also review or reduce limits anytime.

Repayment history is part of your credit file in New Zealand. Missing payments harms, while paying on time maintains your profile. But taking a loan isn’t a shortcut to “improving” credit—focus on affordability and fit.

Personalised quotes may be available in as little as 7 minutes, depending on the information you provide. You’ll need to give accurate details and may need to supply recent bank statements or other documents before a final decision is made.

If you’re looking to compare fixed repayments against overdraft or card options for your next one-off bill, check your rate with Nectar and see if a clear, structured loan fits better than open-ended debt. No pressure—just clear costs and a digital process tuned for practical New Zealanders.

* Nectar Money offers competitive unsecured personal loan rates with fixed interest rates from 7.95% to 29.95% p.a., based on your credit profile. A $240 establishment fee and $1.75 administration fee per repayment apply. Strong Credit borrowers may qualify for low, competitive rates from 7.95% to 16.95% p.a.; Good Credit borrowers may qualify for rates from 16.95% to 22.95% p.a.; and Fair or Developing Credit borrowers may qualify for rates from 24.95% to 29.95% p.a. The broad range helps Nectar offer low interest rates to borrowers with excellent credit, while also providing loan options for more New Zealanders, including borrowers with fair or developing credit profiles. Learn more here.

All loans are subject to responsible lending checks and standard borrowing criteria. Please see our privacy policy and rates and terms, or visit our FAQs for the most up to date information. This publication is provided for general information purposes only and does not constitute legal, tax, financial, or other professional advice from Nectar Money. It is not intended as a substitute for obtaining advice from a financial adviser or any other qualified professional. We make no representations, warranties, or guarantees, whether express or implied, that the content in this publication is accurate, complete, or up to date.