0% APR Credit Cards: Strategies for No Interest Savings

Introduction

Navigating the world of credit cards can be daunting, particularly when it comes to grasping the nuances of 0% APR offers. These appealing credit options present a unique opportunity for consumers to make significant purchases or manage existing debt without the burden of interest during an introductory period.

However, the challenge lies in effectively leveraging these benefits while steering clear of common pitfalls that could result in unexpected costs.

How can individuals ensure they maximise their savings and maintain control over their finances throughout this promotional phase?

Understand 0% APR Credit Cards

A credit card option presents an enticing introductory phase where no interest is charged on purchases or balance transfers. Typically, this lasts around 15 months, with many options offering around 15 months. Currently, certain offerings extend the promotional period for as long as 24 months, providing consumers ample opportunity to save or make purchases without incurring interest. However, cardholders must adhere to the terms; neglecting this obligation could result in the loss of the promotional rate and the onset of interest charges. It is also crucial to understand that not all transactions may qualify for the promotional rate. For instance, while some accounts may apply the 0% rate to purchases and balance transfers, cash advances often do not qualify. Thus, it is essential to fully leverage the benefits of your account and avoid potential pitfalls.

Real-world examples underscore the effectiveness of these credit card options. The U.S. Bank Cash+® Visa Signature® Card, for instance, offers a 0% APR for the first 15 billing cycles, allowing users to earn up to 5% cash back in selected categories. Similarly, the Discover it® Cash Back offer features a 0% APR for 15 months, alongside a cash back program that enhances its appeal. These examples illustrate how consumers can strategically utilize credit options to manage debt or make purchases, provided they comply with the requirements and understand the specific terms. Additionally, setting up automatic payments can help ensure that at least the minimum payment is made on time, further protecting the promotional rate.

Implement Strategies to Maximize 0% APR Benefits

To maximise the benefits of your 0% APR credit card, consider these strategies:

Use Credit Card for Large Purchases: When facing significant expenses, such as home appliances or furniture, leveraging your credit card allows you to spread the cost over several months without accruing interest. This approach can lead to substantial savings compared to traditional financing options.

Debt Consolidation: Transferring existing debt to a 0% APR card can dramatically reduce your interest costs. On average, consumers save hundreds of dollars by consolidating their debt this way. Be mindful of transfer fees, typically ranging from 3% to 5% of the transferred amount, as these can impact your overall savings.

Contribute More Than the Minimum Payment: While making at least the minimum payment is crucial to maintain your 0% APR offer, strive to pay more whenever possible. This proactive strategy ensures your balance is settled before the promotional period concludes, allowing you to benefit from a no interest offer and preventing any interest charges from accruing.

Set Up Alerts: Use your bank’s mobile application to set reminder notifications. This straightforward step helps you stay organised and avoid missed payments, which could jeopardise your 0% APR offer and result in higher interest rates.

Plan Your Spending: Be strategic with your purchases. Utilise the payment method for planned expenses rather than impulsive buys to ensure you can settle the balance on time. This disciplined approach not only safeguards your financial well-being but also maximises the benefits of your 0% APR account.

Maintain a Low Credit Utilisation Ratio: Keep your credit utilisation below 30% to avoid negatively affecting your credit score. High credit utilisation can impact your overall credit health, especially when using credit cards for significant purchases.

Set a Payoff Deadline: Consider establishing a self-imposed deadline for paying off your balance before the promotional period ends. This tactic can enhance your financial decision-making and help you manage your payments effectively.

Avoid Common Mistakes with 0% APR Offers

To avoid common mistakes when utilising credit cards, consider these essential tips:

Overdue Transactions: One of the most significant risks is failing to complete a transaction. This oversight can result in forfeiting your offer and facing high-interest rates, potentially activating a penalty APR if the instalment is overdue by 60 days or more. Always ensure that you pay at least the minimum on time.

Not Reading the Fine Print: Each account comes with specific terms for the offer. Failing to understand these details can lead to unexpected charges, making it crucial to read the fine print carefully.

Overspending: Just because you have a credit card offer does not mean you should spend without restraint. Adhere to a budget to prevent accumulating debt that may become challenging to repay later. For instance, a credit account amount of $5,000 at a 22% APR could take decades to settle if you are only making minimum payments.

Ignoring the End Date: Be mindful of when your promotional period concludes. [Establish a repayment plan](https://theglobeandmail.com/investing/markets/markets-news/Motley Fool/29359469/the-3-worst-mistakes-you-can-make-with-0-apr-credit-cards) to ensure your balance is cleared before this date to avoid incurring interest charges. Setting reminders can assist you in staying on track.

Utilising Credit Cards for Cash Advances: Many credit card options do not apply to cash advances. Using your card for cash withdrawals can lead to high fees, so it is advisable to avoid this practice.

Misconceptions About Outstanding Amounts: Some individuals mistakenly believe that maintaining an outstanding amount benefits their credit score; however, it does not. Always strive to pay off your balance in full to uphold a healthy credit profile.

By adhering to these guidelines, you can make the most of credit options while minimising risks.

Create a Payment Plan to Optimize Savings

To create an effective payment plan for your credit card debt, follow these steps:

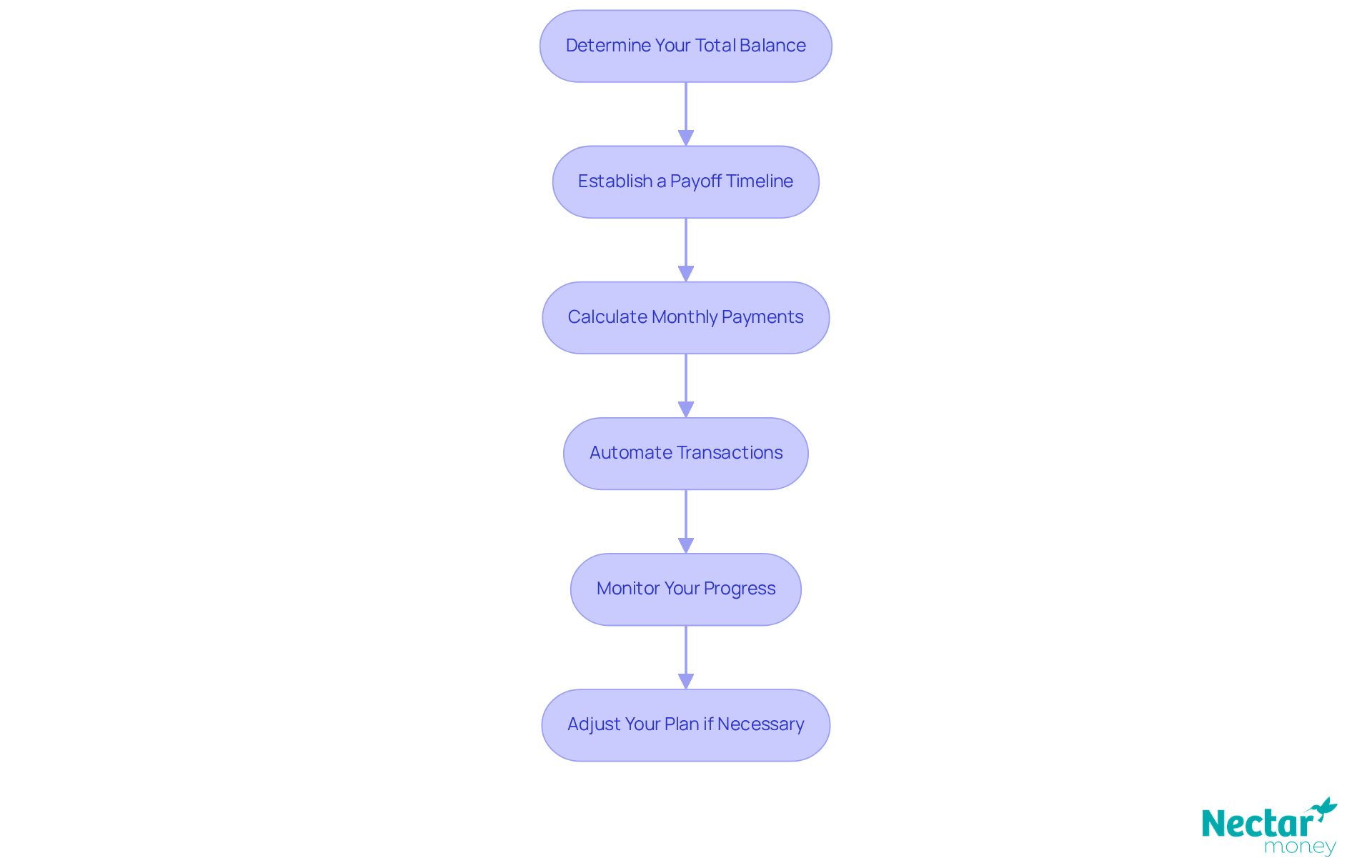

Determine Your Total Balance: Start by calculating the total amount you plan to charge to your 0% APR card. This will give you a clear picture of your debt.

Establish a Timeline: Determine how long you wish to take to settle your balance. Ideally, this should be within the promotional period. Setting a self-imposed deadline, such as one month before the actual deadline, can encourage better financial decisions.

Calculate Monthly Payments: Divide your total amount by the number of months in your promotional period. This will provide you with the monthly amount you need to contribute to your balance. For example, if you have a 12-month 0% APR promotion, think about establishing monthly reminders to monitor your dues.

Automate Transactions: Configure automatic payments to guarantee you never overlook a due date. This will help you stay on track and maintain your 0% APR offer.

Monitor Progress: Regularly check your account to ensure you are on track with your payments. Adjust your plan if necessary to accommodate any changes in your financial situation. Be mindful of the temptation to overspend with your 0% APR offer; only buy items you can afford to settle before the promotional period concludes. Additionally, consider making extra payments to help pay off your balance more effectively.

By following these steps, you can effectively manage your credit card no interest debt and optimize your savings during the promotional period.

Conclusion

Mastering the use of 0% APR credit cards can significantly enhance financial flexibility and savings opportunities. These cards present a unique opportunity to make purchases or transfer balances without incurring interest for a specified introductory period, enabling consumers to manage expenses effectively. By understanding the terms and strategically utilising these offers, cardholders can unlock substantial financial benefits, provided they remain diligent in their payment practises.

To maximise the advantages of 0% APR credit cards, consider:

Using them for large purchases

Transferring high-interest debt

Maintaining a disciplined repayment plan

It is crucial to avoid common pitfalls such as:

Missing payments

Overspending

Neglecting to read the fine print

Implementing proactive measures, such as setting alerts and automating payments, ensures individuals stay on track and fully leverage the benefits of their credit accounts.

Ultimately, the potential for savings with 0% APR credit cards is substantial, but it necessitates careful planning and responsible usage. Embracing these strategies not only aids in managing current expenses but also fosters healthier financial habits for the future. Take full advantage of these offers while being mindful of the associated responsibilities to optimise savings and achieve your financial goals.

Frequently Asked Questions

What is a 0% APR credit card?

A 0% APR credit card offers an introductory period during which no interest is charged on purchases or balance transfers, typically lasting from 12 to 24 months.

How long does the 0% APR promotional period usually last?

The promotional period for 0% APR credit cards typically spans from 12 to 24 months, with many options offering around 15 months.

What happens if I miss a minimum monthly payment on a 0% APR credit card?

If you neglect to make the minimum monthly payments, you could lose the promotional 0% APR rate and start incurring interest charges.

Do all transactions qualify for the 0% APR?

No, not all transactions may qualify for the 0% APR. For example, cash advances often do not qualify, so it’s important to review the terms and conditions.

Can you provide examples of 0% APR credit cards?

Yes, the U.S. Bank Cash+® Visa Signature® Card offers a 0% introductory APR for the first 15 billing cycles and allows users to earn up to 5% cash back in selected categories. The Discover it® Cash Back card also features a 0% introductory APR for 15 months along with a cash back rewards programme.

How can I ensure I maintain the 0% APR promotional rate?

Setting up automatic payments can help ensure that at least the minimum payment is made on time, which protects the promotional rate.

* Nectar Money offers competitive unsecured personal loan rates with fixed interest rates from 9.95% to 29.95% p.a., based on your credit profile. A $240 establishment fee and $1.75 administration fee per repayment apply. Strong Credit borrowers may qualify for low, competitive rates from 9.95% to 16.95% p.a.; Good Credit borrowers may qualify for rates from 16.95% to 22.95% p.a.; and Fair or Developing Credit borrowers may qualify for rates from 24.95% to 29.95% p.a. The broad range helps Nectar offer low interest rates to borrowers with excellent credit, while also providing loan options for more New Zealanders, including borrowers with fair or developing credit profiles. Learn more here.

All loans are subject to responsible lending checks and standard borrowing criteria. Please see our privacy policy and rates and terms, or visit our FAQs for the most up to date information. This publication is provided for general information purposes only and does not constitute legal, tax, financial, or other professional advice from Nectar Money. It is not intended as a substitute for obtaining advice from a financial adviser or any other qualified professional. We make no representations, warranties, or guarantees, whether express or implied, that the content in this publication is accurate, complete, or up to date.