Navigating the world of credit can indeed be daunting, particularly with the vast array of options available to consumers today. Among these, zero interest rate credit cards emerge as a potent financial tool capable of facilitating debt management and delivering substantial savings. However, while these cards offer an appealing opportunity to ease financial burdens, they also introduce their own set of challenges and potential pitfalls.

What strategies can individuals implement to fully leverage the advantages of these financial products while steering clear of common mistakes?

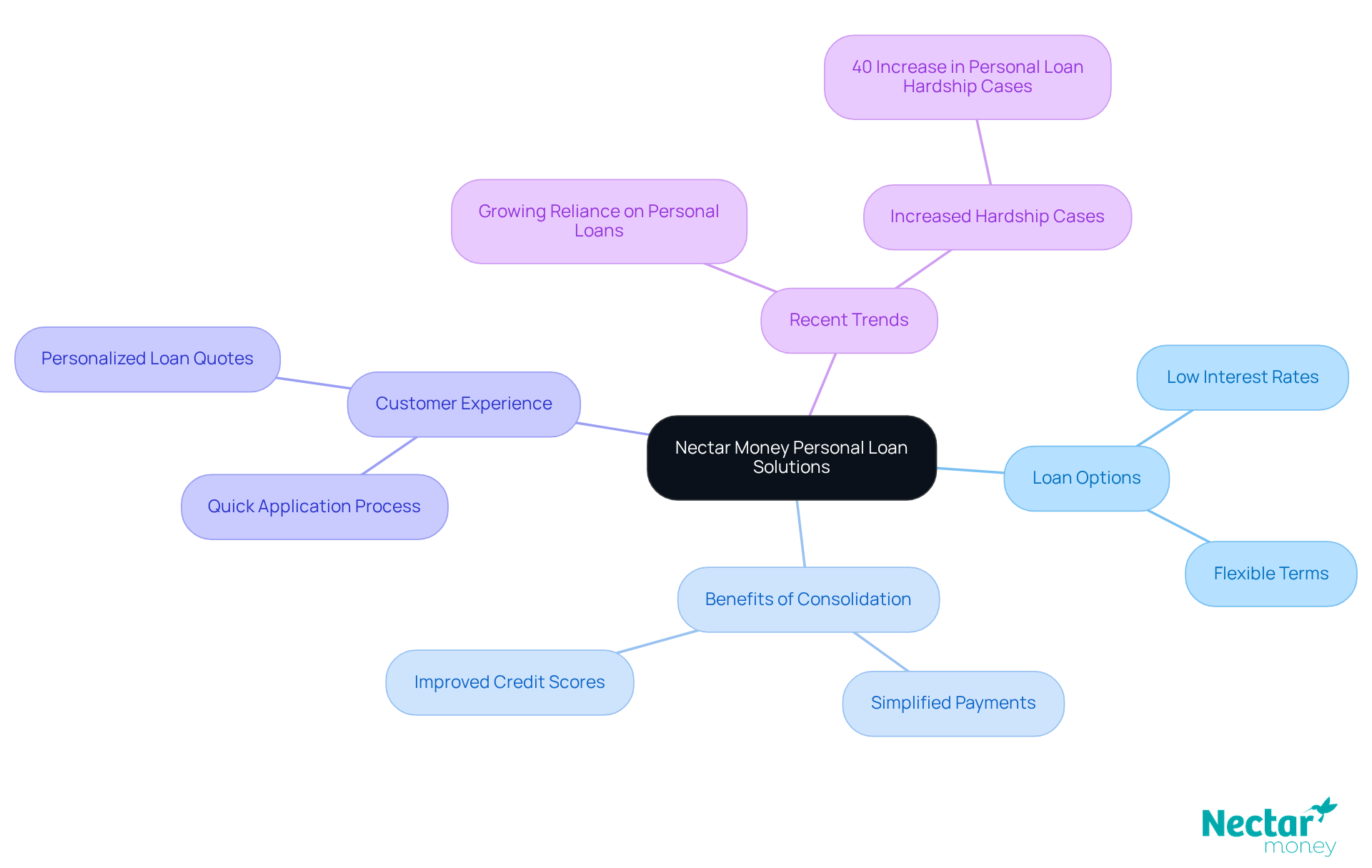

Nectar Money offers a diverse array of personal loan solutions designed specifically for efficient financial management. This allows borrowers to consolidate multiple obligations into a single, manageable payment. With these loans, customers can swiftly access funds to cover expenses, simplifying their repayment process and bolstering their financial stability. This consolidation strategy not only streamlines payments but also has a positive impact by reducing overall liabilities.

Recent trends indicate a growing reliance on personal loans for financial relief, as individuals seek to navigate rising living costs and financial pressures. The straightforward application process enables borrowers to receive personalised loan quotes in just seven minutes, making it an appealing choice for those aiming to improve their financial situation.

Financial advisors emphasise the importance of responsible borrowing, highlighting that this method can enhance credit ratings when managed responsibly. Companies are innovating in this landscape by prioritising customer needs and leveraging technology to provide efficient solutions, ultimately transforming the consolidation experience for many Kiwis.

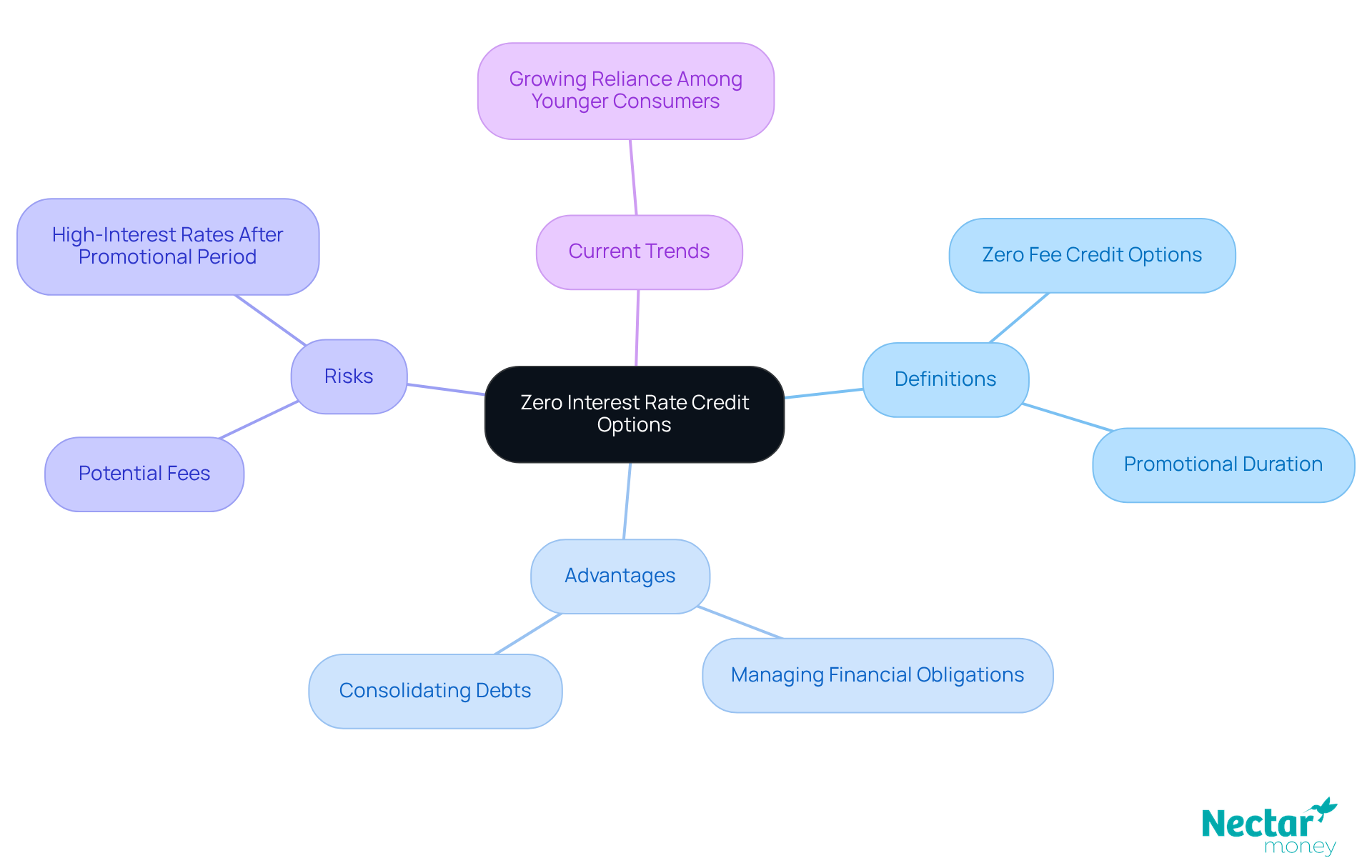

Zero interest rate credit cards are financial instruments that enable consumers to obtain funds without incurring charges for a specified promotional duration, typically lasting from six to twelve months. This feature can be particularly advantageous for managing debt, as it allows borrowers to clear existing balances without incurring extra costs. For instance, individuals consolidating credit card debt can transfer their balances to a no-cost option, effectively halting any charges and allowing them to focus on repayment.

However, it is crucial to understand the terms and conditions associated with these products. Many cards come with specific fees, such as transaction fees or annual fees, which can diminish overall savings. Furthermore, if the balance is not paid off before the promotional period concludes, the remaining amount may incur high-interest rates, often averaging around 20.8% in 2025.

Current trends indicate a growing reliance on zero-fee credit options, particularly among consumers who are becoming increasingly comfortable with credit. Financial experts stress that while these instruments can provide significant short-term relief, they also carry risks if not managed properly. For example, a consumer who transfers a balance but fails to pay it off during the promotional phase may face substantial fees, undermining the initial benefits.

In conclusion, zero interest rate credit cards can serve as a powerful tool for financial management when utilized judiciously. They present a unique opportunity to alleviate financial burdens, but consumers must remain vigilant regarding the terms and potential pitfalls to fully capitalize on their advantages.

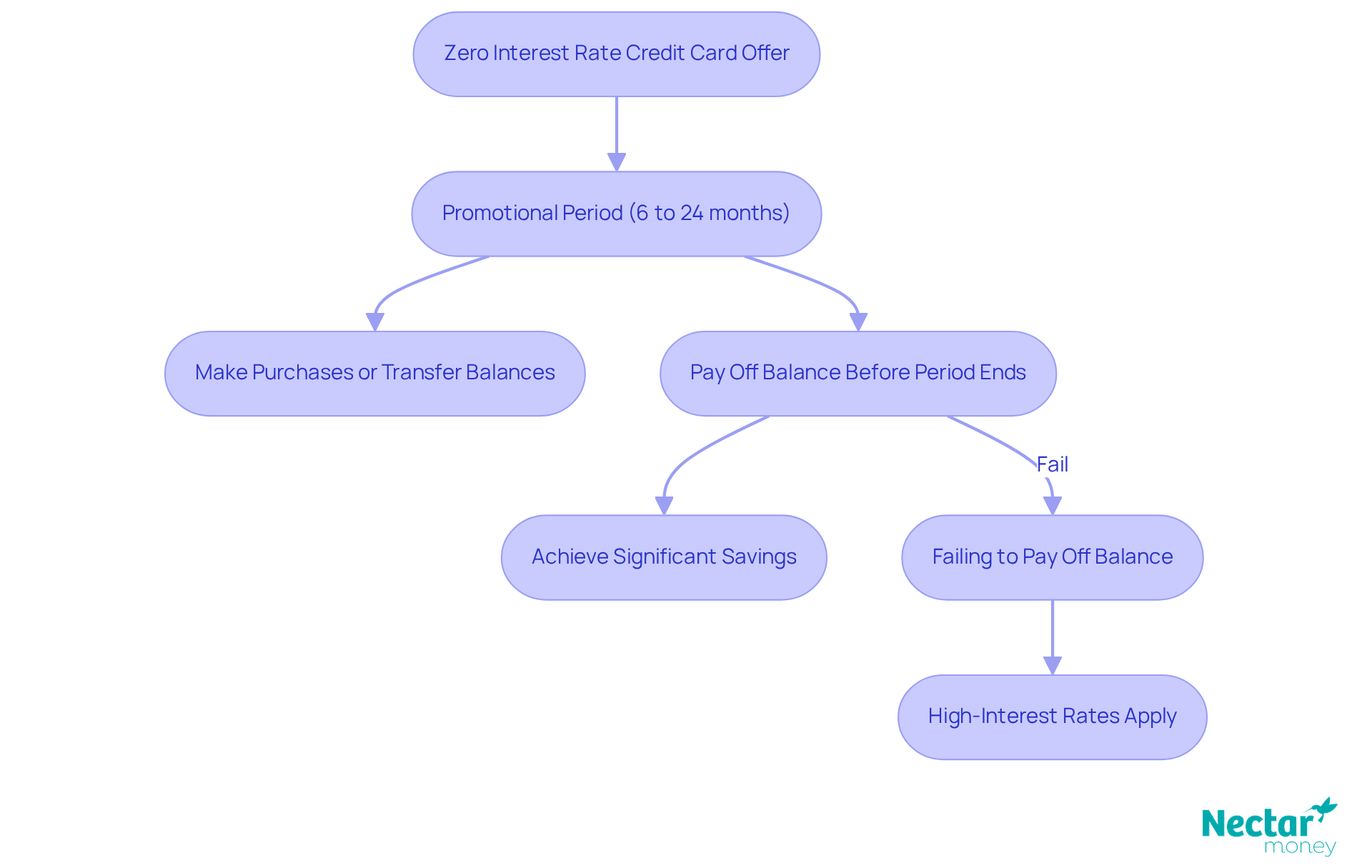

Zero interest rate credit cards often come with zero financing rates that apply to balance transfers or new purchases for a limited duration, typically ranging from six to 24 months. This promotional period allows borrowers to reduce their obligations without incurring charges, leading to significant savings. However, it is essential to make payments before the promotional period expires. Failing to do so can result in high-interest rates that may take effect thereafter. Take control of your finances and make the most of this opportunity.

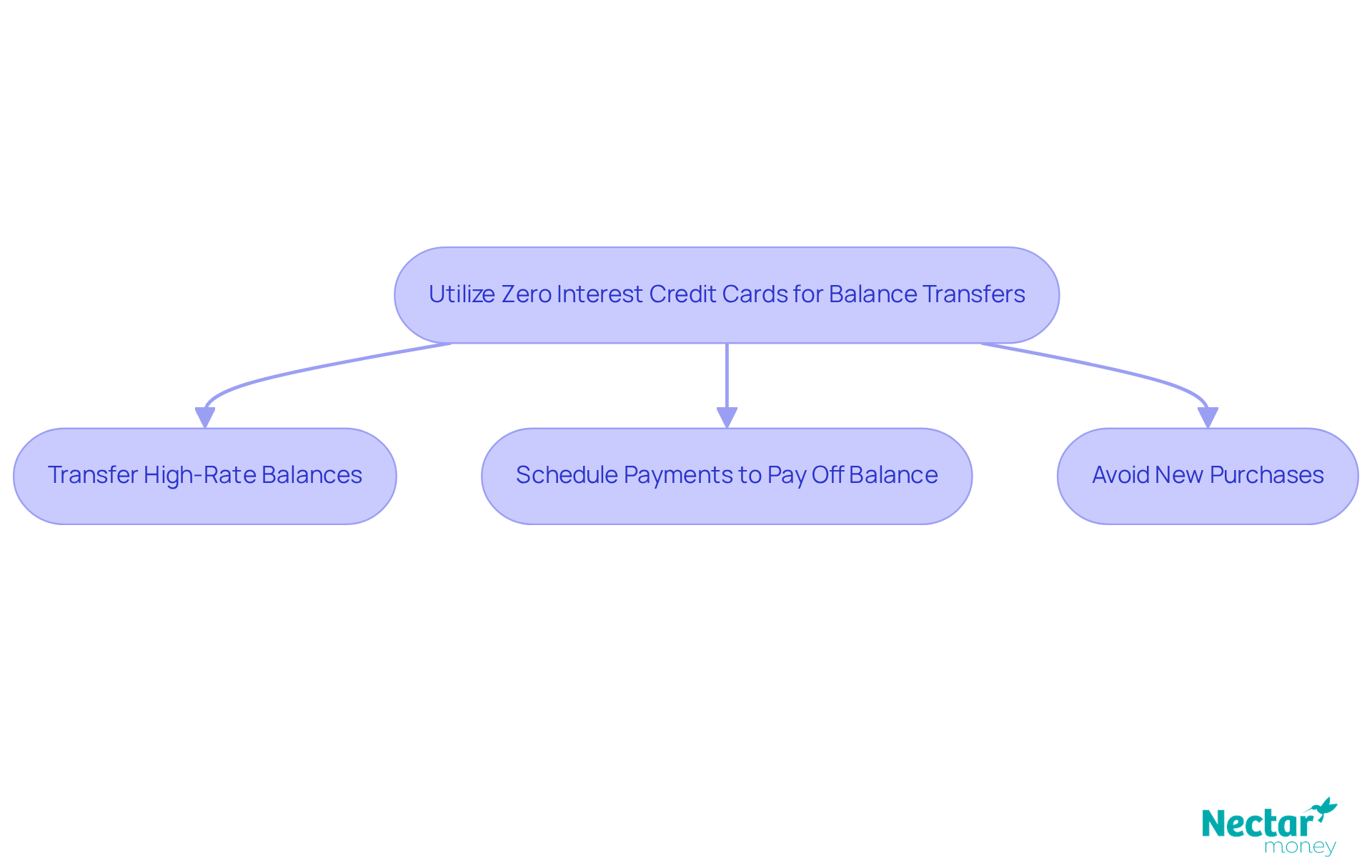

To optimise your savings with zero interest credit cards, consider transferring balances from other accounts to a new card. This strategy allows you to pay down debt more efficiently without incurring additional charges. Additionally, make sure to ensure the balance is fully paid off before the promotional period ends. Avoid making new purchases during this time to prevent finance charges from accumulating.

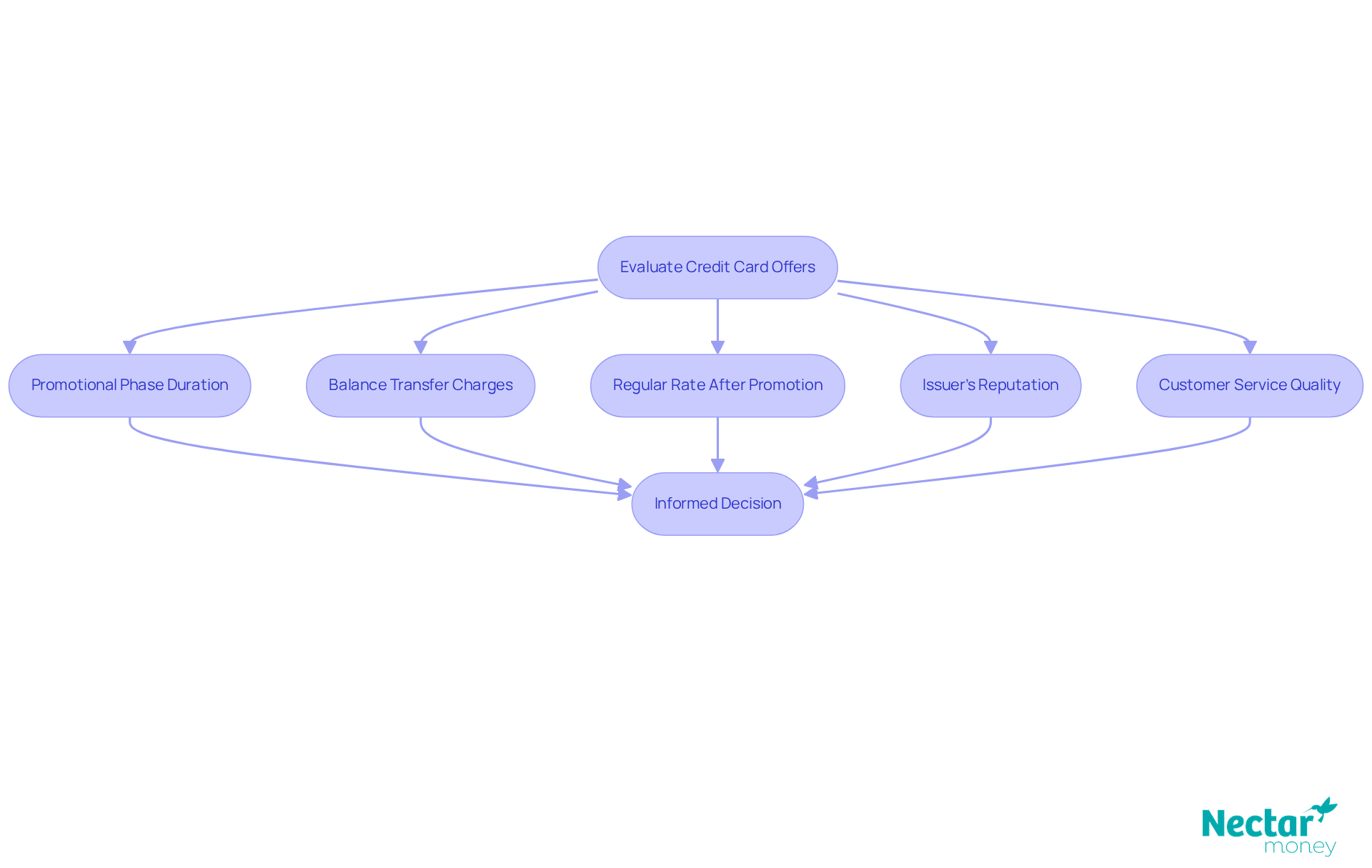

When assessing credit card offers, it is crucial to consider several key elements.

By taking these considerations into account, you can make a more informed decision that aligns with your financial goals.

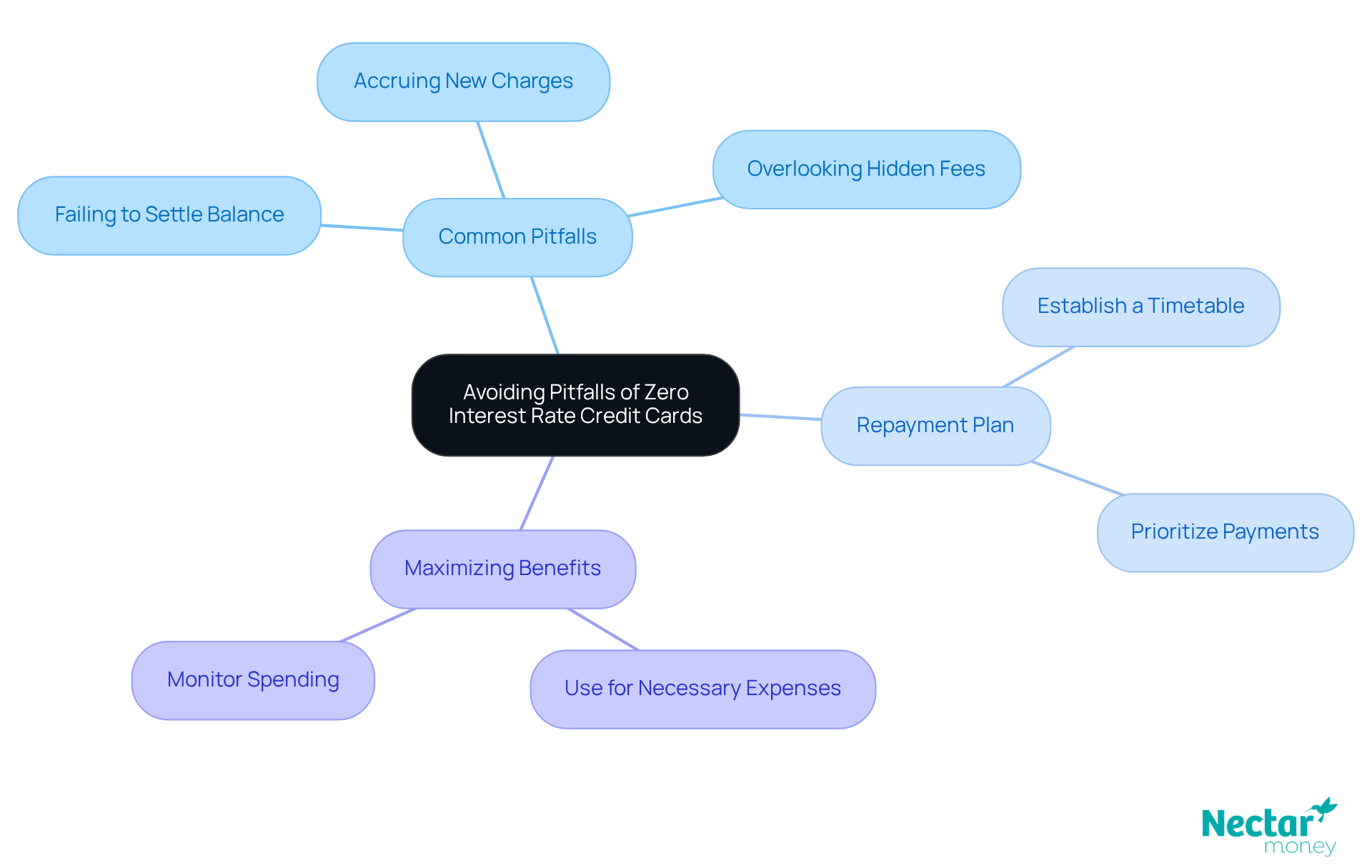

Common pitfalls in utilising zero interest rate credit cards include:

To circumvent these issues, it is crucial to establish a budget and adhere to it diligently. Prioritising the payment of the balance will help ensure that you avoid these pitfalls.

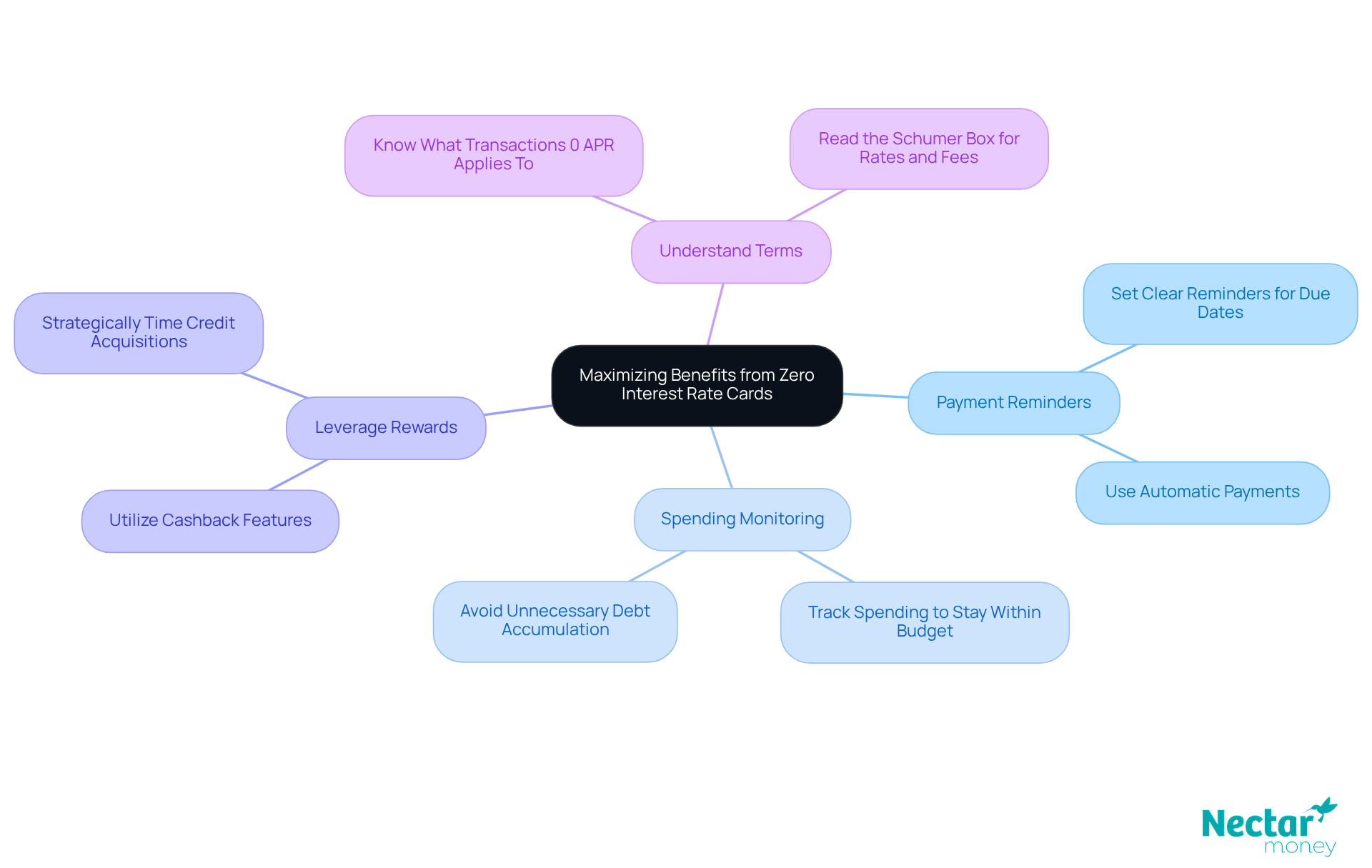

To fully harness the benefits of zero interest rate credit cards, it is essential to use them judiciously for both scheduled purchases and emergencies. Start by establishing clear reminders for payment due dates to ensure deadlines are met, as even a single late payment can result in the cancellation of your promotional rate. Monitoring your spending is vital; this practice helps you stay within your budget and avoid unnecessary debt accumulation.

Leveraging rewards or cashback features can further amplify your savings. Numerous no-fee financial products offer these benefits, potentially yielding extra savings or perks when utilized strategically. For instance, a well-timed credit acquisition can aid in debt management, as evidenced by case studies that highlight the effectiveness of these strategies.

Moreover, it is important that consumers familiarize themselves with the specific terms of their no-cost offers. It is crucial to understand whether the promotional rate applies to purchases, balance transfers, or both, as this knowledge is key to maximizing the potential of the account. By implementing these strategies, individuals can not only manage their finances more effectively but also capitalize on the unique advantages that zero interest rate cards present, particularly in relation to financial goals.

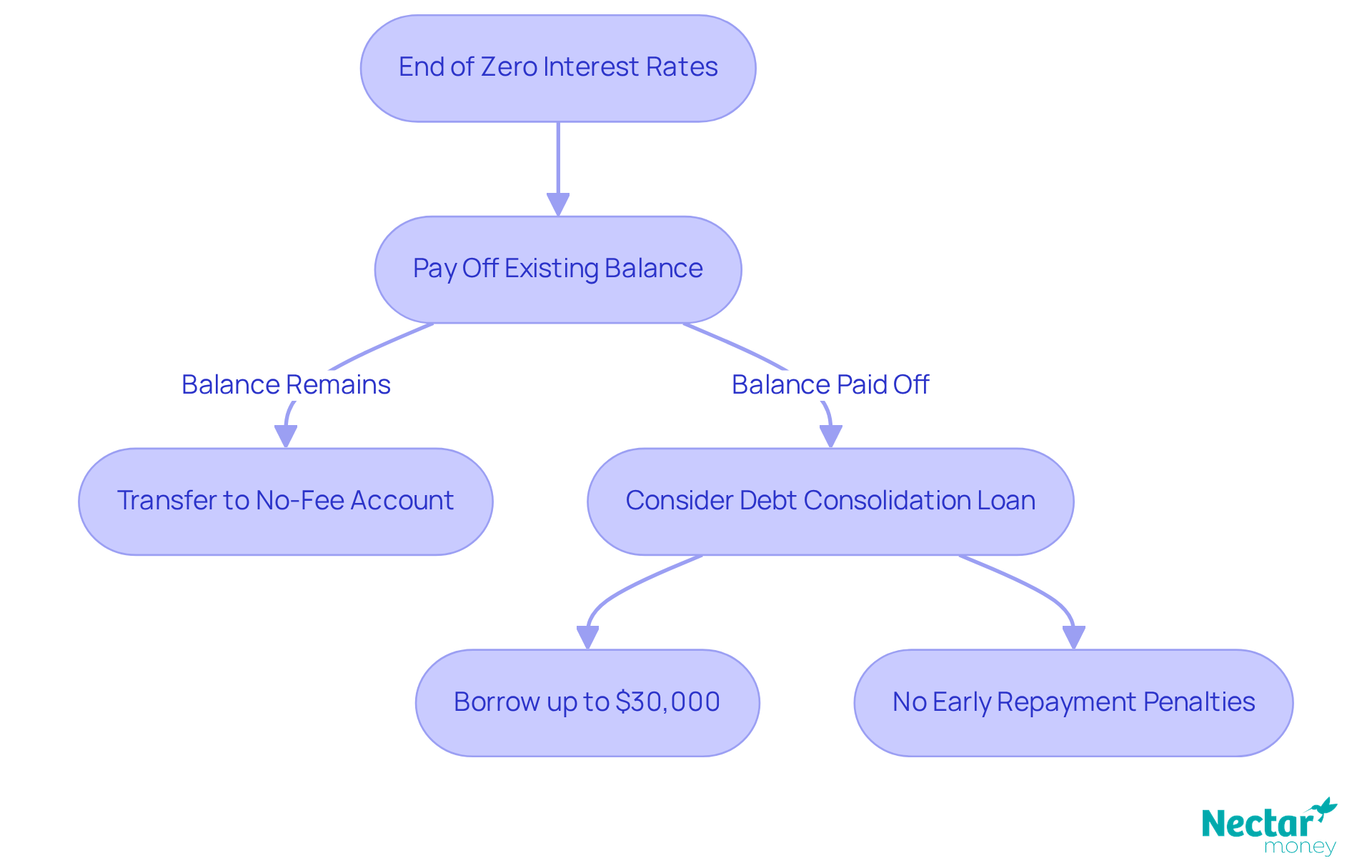

As the promotional phase for no-cost rates comes to a close, having a well-defined strategy is paramount. First, ensure that any existing balance is paid off to avoid incurring high-interest charges. If a balance remains, consider transferring it to another no-fee account or exploring alternative financial management options, such as personal loans.

With the capacity to consolidate debts and reduce monthly payments, a balance transfer can streamline your debt obligations by merging multiple debts into one manageable payment. This method not only aids in reducing costs but also aligns your repayment schedule with your income, facilitating better control over your financial situation.

When evaluating credit cards against other financial offerings, it is crucial to consider factors such as rates, charges, and repayment conditions. Personal loans, for instance, may provide fixed rates and lower overall costs. This makes them a viable choice for consolidating debt or addressing significant expenses.

While credit cards offer flexibility, they require diligent oversight to avoid potential drawbacks. Assess your financial circumstances and objectives to identify the most suitable option for your needs, whether it involves leveraging Nectar Money’s services or opting for a no-cost credit alternative.

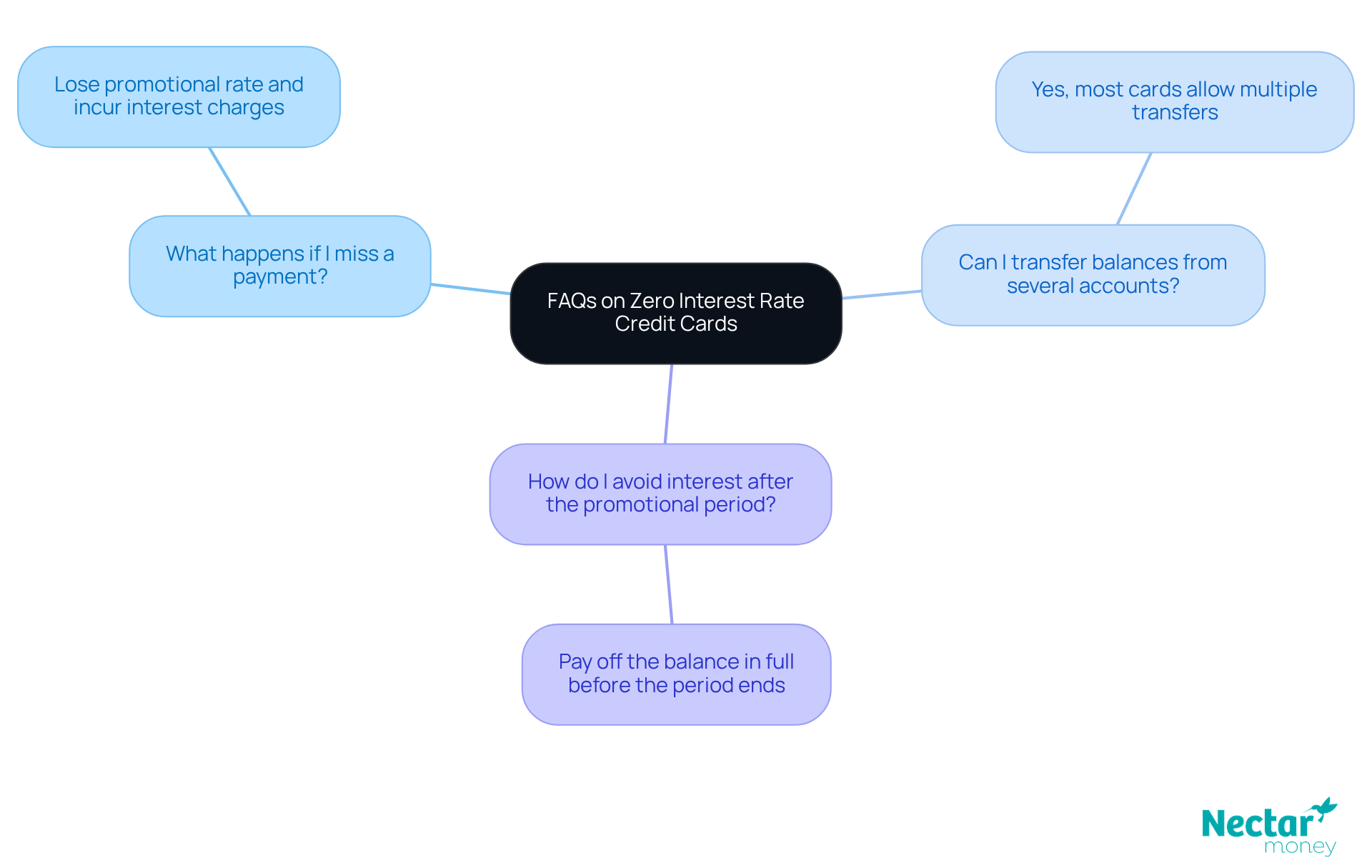

Common inquiries regarding zero interest rate credit cards often arise. What happens if I miss a payment? Typically, you may lose the promotional rate and incur interest charges. Can I transfer balances from several accounts? Yes, most cards allow balance transfers. How do I manage my payments after the promotional period? Pay off the balance in full before the promotional period ends. Financial literacy is essential; it empowers consumers to navigate their options, such as credit card offers, more effectively.

Utilising zero interest rate credit cards can significantly enhance financial management when approached with careful planning and awareness. These financial tools present an opportunity to alleviate debt burdens, particularly when used for balance transfers or consolidating high-interest loans. However, grasping the nuances of these offers is imperative to avoid potential pitfalls that could negate their benefits.

Key strategies include:

Evaluating various credit card offers based on fees, duration of promotional rates, and issuer reputation can lead to more informed financial decisions. By implementing these strategies, individuals can maximise the advantages of zero interest rate credit cards while maintaining a healthy financial trajectory.

In a broader context, the effective use of zero interest rate cards not only facilitates immediate financial relief but also contributes to long-term financial stability. As consumers navigate their options, remaining informed and proactive is essential. Embracing a strategic approach to credit management empowers individuals to make sound financial choices, whether through zero interest rate cards or alternative solutions like personal loans from Nectar Money. The journey to financial wellness begins with informed decisions and a commitment to responsible borrowing.

What personal loan solutions does Nectar Money offer?

Nectar Money provides a variety of personal loan options aimed at efficient financial management, allowing borrowers to consolidate multiple debts into a single, manageable payment.

What are the interest rates for Nectar Money loans?

Interest rates for Nectar Money loans start at 11.95% per annum.

How can personal loans from Nectar Money benefit borrowers?

These loans can help eliminate high-interest debts, simplify repayment processes, and improve financial stability, while also potentially enhancing credit scores by reducing overall liabilities.

What is the application process like for Nectar Money loans?

The application process is straightforward, enabling borrowers to receive personalised loan quotes in just seven minutes.

Why are personal loans becoming popular in New Zealand?

There is a growing reliance on personal loans for financial consolidation in New Zealand as individuals seek to manage rising living costs and financial pressures.

What are zero interest rate credit options?

Zero interest rate credit options are financial instruments that allow consumers to obtain funds without incurring charges for a promotional period, typically lasting six to twelve months.

How can zero interest rate credit options help with debt management?

These options enable borrowers to transfer high-rate credit balances to a no-cost option, stopping extra charges and allowing them to focus on repayment.

What should consumers be cautious about with zero interest rate credit options?

Consumers should understand the terms and conditions, as many offers may include specific fees, and failing to pay off the balance before the promotional period ends can lead to high-interest rates.

What are the potential risks of using zero interest rate credit cards?

If a balance is not paid off during the promotional phase, consumers may face substantial fees and high-interest rates that can undermine the benefits of the initial offer.

How long do zero interest rates typically last on credit cards?

Zero interest rates usually apply for a limited duration ranging from six to 24 months.

* A Nectar Money loan requires responsible borrowing checks and must meet standard borrowing criteria. Interest rates 9.95% - 29.95% p.a. fixed. $240 establishment fee and $1.75 admin fee per repayment apply. Please see our privacy policy and rates and terms or visit our FAQs for the most up to date information. This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Nectar Money, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.